The Dividend Investing Resource Center

Discover how Dividend Reinvestment Plans (DRIPs) can amplify your investment portfolio by automatically reinvesting company dividends into additional shares.

By leveraging the power of compounding, you can escalate your shareholdings over time.

What is dividend investing?

Dividend investing is a means of building wealth over a long period of time with reduced risk.

Many brokers offer fee-free purchases and reinvestments and the ability to reinvest fractional shares.

Dividend investing is for the long term buy-and-hold type investor who wants to sleep at night while their investments steadily build.

What is DRIP?

The term DRIP is an abbreviation for dividend reinvestment plans, which offer investors the opportunity to reinvest all, or a portion, of their dividend payments back into a company’s stock. Oftentimes, companies will allow investors to purchase additional shares of stock through these programs too.

What is DRIP investing?

Dividend reinvestment plans are sponsored by companies that allow individual investors to purchase common stock without going through a broker. The name comes from the plan’s policy of allowing the investor to automatically reinvest dividends to purchase additional shares of stock.

Many DRIPs are offered to investors free of any participation costs, while others charge relatively small administration fees or commissions. While the name implies these plans are limited to reinvesting stock dividends, some plans allow participants to directly purchase a company’s stock. This enhanced practice is sometimes referred to as optional cash purchases or OCPs.

Advantages of DRIP

A large number of companies offer dividend reinvestment programs, and participation rules are usually outlined in the investor section of the company’s website. Since these plans are flexible enough to allow even small purchases without a broker’s fee, it’s hard to find any downside to these offerings. In fact, there are several significant advantages of these programs including:

Low cost of entry

Investors don’t need a lot of money to enroll in these programs.

Most companies allow the purchase of just a single share of stock, and often this purchase is at a discount.

Cost-effective

Since the investor isn’t paying brokerage fees, all of the money is put to work.

Over 100 companies allow investors to purchase stock at a discount to the current market price through optional cash purchase plans, or OCPs.

DCA

Finally, many of the DRIPs allow investors to purchase stock through automated weekly or monthly deductions.

This long-term purchase strategy provides the investor with a less painful, and more structured, approach to buying stocks.

CCC list

Most Popular Dividend Stocks

Here are some of the top-performing and most popular dividend stocks.

| Logo | Symbol | Stock Type | Company | Sector | Industry | Price | Div Yield | 5Y Avg Yield | Current Div | Payouts/Year | Annualized | Previous Div | Ex-Date | Pay-Date | Low | High | Chowder Number | DGR 1Y | DGR 3Y | DGR 5Y | DGR 10Y | TTR 1Y | TTR 3Y | FV (Peter Lynch) | FV (Peter Lynch) % | EPS 1Y | Revenue 1Y | NPM | CF/Share | ROE | Current R | Debt/Capital | ROTC | P/E | P/BV | PEG |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

| VST | Challenger | Vistra Corp. | Utilities | Utilities – Independent Power Producers | $148.19 | 0.62% | 1.55% | $0.229 | 4 | $0.916 | $0.228 | Sep 21, 2026 | Sep 30, 2026 | $132.66 | $219.82 | 10.4 | 2.1% | 5.3% | 9.8% | — | -28.0% | 76.5% | $53.94 | 175.0% | 0.0% | 3.0% | 10.5% | $13.85 | 42.9% | 0.9 | 85.0% | 10.8% | 24.7x | 16.1x | 0.44 |

|

| AVGO | Contender | Broadcom Inc. | Technology | Semiconductors | $427.95 | 0.61% | 1.63% | $0.650 | 4 | $2.600 | $0.650 | Jun 22, 2026 | Jun 30, 2026 | $281.87 | $495.00 | 13.2 | 10.4% | 12.4% | 12.6% | 29.9% | 42.2% | 74.3% | $29.95 | 1,329.0% | 0.0% | 23.9% | 38.9% | $7.07 | 37.3% | 2.2 | 42.0% | 20.5% | 71.4x | 23.2x | 0.48 |

|

| LRCX | Contender | Lam Research Corporation | Technology | Semiconductor Equipment & Materials | $308.49 | 0.34% | 0.94% | $0.260 | 4 | $1.040 | $0.260 | Jun 17, 2026 | Jul 8, 2026 | $94.11 | $438.50 | 15.2 | 13.0% | 14.7% | 14.9% | 24.1% | 205.9% | 66.7% | $28.80 | 971.0% | 0.0% | 26.0% | 31.3% | $4.68 | 65.1% | 2.6 | — | 52.2% | 53.6x | 36.5x | 1.45 |

|

| AMAT | Challenger | Applied Materials, Inc. | Technology | Semiconductor Equipment & Materials | $507.67 | 0.42% | 0.78% | $0.530 | 4 | $2.120 | $0.460 | Aug 20, 2026 | Sep 10, 2026 | $154.47 | $739.67 | 16.7 | 15.1% | 20.2% | 16.2% | 16.9% | 185.2% | 52.3% | $53.05 | 857.0% | 0.0% | 4.4% | 29.3% | $10.07 | 39.7% | 2.5 | 20.0% | 30.6% | 47.9x | 16.9x | 1.28 |

|

| GS | Contender | Goldman Sachs Group, Inc. (The) | Financial Services | Capital Markets | $1,039.32 | 1.73% | 2.33% | $4.500 | 4 | $18.000 | $4.500 | Sep 1, 2026 | Sep 29, 2026 | $705.55 | $1,153.99 | 29.5 | 41.7% | 19.3% | 27.7% | 20.7% | 49.4% | 49.3% | $323.85 | 221.0% | 0.0% | — | 31.0% | $-135.17 | 16.9% | 1.6 | 77.0% | — | 16.1x | 2.8x | 1.48 |

|

| CAT | Champion | Caterpillar, Inc. | Industrials | Farm & Heavy Construction Machinery | $814.81 | 0.80% | 1.65% | $1.630 | 4 | $6.520 | $1.510 | Jul 20, 2026 | Aug 19, 2026 | $405.46 | $1,073.46 | 8.8 | 7.3% | 7.9% | 8.0% | 7.2% | 93.2% | 44.9% | $100.20 | 713.0% | 0.0% | — | 13.3% | — | 51.3% | 1.4 | 62.0% | — | 40.7x | 20.1x | 1.91 |

|

| RTX | Champion | RTX Corporation | Industrials | Aerospace & Defense | $226.24 | 1.29% | 2.05% | $0.730 | 4 | $2.920 | $0.680 | Aug 14, 2026 | Sep 3, 2026 | $150.61 | $226.88 | 8.7 | 7.8% | 7.3% | 7.4% | 5.5% | 50.2% | 41.4% | $28.45 | 695.0% | 0.0% | 9.7% | 8.3% | $10.54 | 12.3% | 1.0 | 33.0% | 7.6% | 39.8x | 4.6x | 2.77 |

|

| MS | Contender | Morgan Stanley | Financial Services | Capital Markets | $216.63 | 2.12% | 3.23% | $1.150 | 4 | $4.600 | $1.000 | Jul 31, 2026 | Aug 14, 2026 | $141.03 | $232.25 | 21.0 | 9.9% | 9.3% | 18.9% | 20.4% | 57.7% | 40.3% | $61.85 | 250.0% | 0.0% | 14.4% | 25.1% | $-9.92 | 18.0% | 2.0 | 79.0% | 4.2% | 17.5x | 3.2x | 2.05 |

|

| MFC | Contender | Manulife Financial Corporation | Financial Services | Insurance – Life | $44.40 | 1.59% | 4.29% | $0.352 | 2 | $0.704 | $0.354 | Aug 21, 2026 | Sep 21, 2026 | $29.70 | $45.33 | -2.7 | -41.3% | -12.1% | -4.3% | 2.8% | 52.8% | 37.3% | $13.15 | 238.0% | 0.0% | 14.4% | 20.3% | $18.62 | 13.3% | 29.5 | 23.0% | 11.0% | 16.9x | 2.0x | 0.78 |

|

| CSCO | Contender | Cisco Systems, Inc. | Technology | Communication Equipment | $123.46 | 1.36% | 2.82% | $0.420 | 4 | $1.680 | $0.420 | Jul 6, 2026 | Jul 22, 2026 | $65.75 | $130.37 | 4.0 | 2.5% | 2.5% | 2.6% | 5.9% | 77.9% | 36.4% | $15.00 | 723.0% | 0.0% | 5.3% | 20.1% | $3.30 | 25.2% | 0.9 | 28.0% | 17.8% | 41.2x | 10.0x | 1.19 |

|

| RY | Contender | Royal Bank Of Canada | Financial Services | Banks – Diversified | $212.41 | 1.76% | 3.39% | $1.249 | 3 | $3.747 | $1.200 | Jul 27, 2026 | Aug 24, 2026 | $132.51 | $218.57 | -4.5 | -42.5% | -14.5% | -6.3% | 0.1% | 64.1% | 35.2% | $54.90 | 287.0% | 0.0% | 16.2% | 31.0% | $-44.16 | 16.2% | — | 74.0% | 4.5% | 19.4x | 3.2x | 2.35 |

|

| JPM | Contender | JP Morgan Chase & Co. | Financial Services | Banks – Diversified | $351.79 | 1.71% | 2.51% | $1.500 | 4 | $6.000 | $1.500 | Jul 6, 2026 | Jul 31, 2026 | $279.10 | $359.30 | 12.5 | 13.2% | 14.5% | 10.8% | 12.8% | 26.0% | 34.7% | $116.60 | 202.0% | 0.0% | — | 34.9% | — | 17.8% | — | — | — | 15.1x | 2.6x | 1.72 |

|

| LLY | Contender | Eli Lilly and Company | Healthcare | Drug Manufacturers – General | $1,213.91 | 0.57% | 0.81% | $1.730 | 4 | $6.920 | $1.730 | Aug 14, 2026 | Sep 10, 2026 | $625.90 | $1,249.45 | 15.8 | 15.4% | 15.2% | 15.2% | 12.3% | 96.4% | 33.7% | $148.80 | 716.0% | 0.0% | 44.7% | 33.5% | $31.49 | 102.3% | 1.4 | 59.0% | 37.6% | 40.8x | 34.8x | 1.49 |

|

| MPLX | Contender | MPLX LP | Energy | Oil & Gas Midstream | $58.73 | 7.34% | 9.75% | $1.077 | 4 | $4.308 | $1.077 | Aug 7, 2026 | Aug 14, 2026 | $47.80 | $60.95 | 16.7 | 12.5% | 11.6% | 9.4% | 8.1% | 35.2% | 32.1% | $23.25 | 153.0% | 0.0% | 8.9% | 36.4% | $0.00 | — | — | 64.0% | 12.1% | 12.6x | 4.2x | 3.27 |

|

| PM | Contender | Philip Morris International Inc | Consumer Defensive | Tobacco | $187.65 | 3.13% | 4.63% | $1.470 | 4 | $5.880 | $1.470 | Jun 25, 2026 | Jul 20, 2026 | $142.11 | $207.76 | 7.3 | 8.9% | 5.0% | 4.1% | 3.7% | 17.8% | 31.5% | $36.40 | 416.0% | 0.0% | 7.3% | 25.6% | $9.15 | — | 1.0 | 1.3% | 32.4% | 25.8x | —x | 2.47 |

|

| PNC | Contender | PNC Financial Services Group, I | Financial Services | Banks – Regional | $251.85 | 3.18% | 3.83% | $2.000 | 4 | $8.000 | $1.700 | Jul 20, 2026 | Aug 5, 2026 | $176.88 | $258.13 | 11.8 | 9.2% | 5.5% | 8.6% | 13.1% | 41.0% | 31.2% | $90.80 | 177.0% | 0.0% | 7.2% | 29.0% | $18.77 | 12.6% | — | 57.0% | 5.6% | 13.9x | 1.8x | 1.98 |

|

| WMT | King | Walmart Inc. | Consumer Defensive | Discount Stores | $111.20 | 0.89% | 1.14% | $0.248 | 4 | $0.992 | $0.248 | Aug 21, 2026 | Jan 4, 2027 | $95.42 | $135.16 | 6.8 | 9.0% | 8.6% | 5.9% | 3.9% | 14.8% | 29.7% | $14.20 | 683.0% | 0.0% | 4.7% | 3.2% | $5.14 | 24.1% | 0.8 | 38.0% | 15.1% | 39.2x | 9.4x | 4.24 |

|

| KMI | Challenger | Kinder Morgan, Inc. | Energy | Oil & Gas Midstream | $32.18 | 3.70% | 5.54% | $0.298 | 4 | $1.192 | $0.293 | Aug 3, 2026 | Aug 17, 2026 | $25.60 | $34.81 | 0.0 | -23.9% | -7.6% | -3.7% | 0.0% | 21.3% | 29.5% | $7.75 | 315.0% | 0.0% | 12.2% | 19.3% | $2.94 | 11.0% | 0.5 | 48.0% | 5.6% | 20.8x | 2.3x | 3.50 |

|

| BAC | Contender | Bank of America Corporation | Financial Services | Banks – Diversified | $61.95 | 1.81% | 2.37% | $0.280 | 4 | $1.120 | $0.280 | Sep 4, 2026 | Sep 25, 2026 | $44.75 | $62.99 | 11.0 | 7.7% | 8.4% | 9.2% | 18.8% | 41.1% | 29.4% | $21.65 | 186.0% | 0.0% | — | 29.5% | — | 11.2% | — | — | — | 14.3x | 1.6x | 1.06 |

|

| PSX | Contender | Phillips 66 | Energy | Oil & Gas Refining & Marketing | $210.35 | 2.42% | 3.58% | $1.270 | 4 | $5.080 | $1.270 | Aug 18, 2026 | Sep 1, 2026 | $118.07 | $216.08 | 8.9 | 6.2% | 6.9% | 6.5% | 7.9% | 86.9% | 27.7% | $87.60 | 140.0% | 0.0% | -6.1% | 4.5% | $22.26 | 23.5% | 1.3 | 37.0% | 14.8% | 12.0x | 3.0x | 1.18 |

|

| MO | King | Altria Group, Inc. | Consumer Defensive | Tobacco | $68.35 | 6.20% | 8.38% | $1.060 | 4 | $4.240 | $1.060 | Jun 15, 2026 | Jul 10, 2026 | $54.70 | $77.06 | 10.5 | 3.9% | 4.1% | 4.3% | 6.5% | 20.8% | 27.6% | $23.75 | 188.0% | 0.0% | -1.5% | 39.0% | $5.63 | — | 0.5 | 1.1% | 38.3% | 14.4x | —x | 1.55 |

|

| ASB | Contender | Associated Banc-Corp | Financial Services | Banks – Regional | $31.35 | 3.06% | 3.86% | $0.240 | 4 | $0.960 | $0.240 | Sep 1, 2026 | Sep 15, 2026 | $23.74 | $32.00 | 8.8 | 4.4% | 4.6% | 5.7% | 8.2% | 39.5% | 25.3% | $14.30 | 119.0% | 0.0% | 43.3% | 31.5% | $3.81 | 9.7% | — | 14.0% | 8.2% | 11.0x | 1.1x | 1.78 |

|

| ABBV | Contender | AbbVie Inc. | Healthcare | Drug Manufacturers – General | $250.94 | 2.76% | 3.74% | $1.730 | 4 | $6.920 | $1.730 | Jul 15, 2026 | Aug 14, 2026 | $190.75 | $267.47 | 8.9 | 5.6% | 5.3% | 6.1% | 11.9% | 36.1% | 24.3% | $17.70 | 1,318.0% | 0.0% | 8.6% | 9.8% | $0.00 | — | — | 1.1% | 10.7% | 70.9x | —x | 0.41 |

|

| USB | Contender | U.S. Bancorp | Financial Services | Banks – Regional | $64.03 | 2.44% | 4.41% | $0.520 | 3 | $1.560 | $0.520 | Jun 30, 2026 | Jul 15, 2026 | $44.34 | $65.02 | 6.8 | 4.0% | 2.7% | 4.4% | 7.4% | 53.2% | 24.1% | $25.05 | 156.0% | 0.0% | 4.8% | 26.3% | $8.04 | 12.6% | — | 49.0% | 6.5% | 12.8x | 1.7x | 2.14 |

|

| OMF | Challenger | OneMain Holdings, Inc. | Financial Services | Credit Services | $62.58 | 6.71% | 9.33% | $1.050 | 4 | $4.200 | $1.050 | Aug 10, 2026 | Aug 14, 2026 | $45.78 | $71.93 | -4.1 | 0.7% | 2.4% | -10.8% | — | 27.2% | 23.5% | $33.15 | 89.0% | 0.0% | 9.7% | 15.3% | $28.09 | 23.3% | — | 87.0% | 3.0% | 9.4x | 2.1x | 0.75 |

|

| GILD | Contender | Gilead Sciences, Inc. | Healthcare | Drug Manufacturers – General | $133.29 | 2.46% | 3.46% | $0.820 | 4 | $3.280 | $0.820 | Sep 15, 2026 | Sep 29, 2026 | $108.46 | $157.29 | 5.4 | 3.2% | 2.8% | 3.0% | 6.2% | 17.3% | 23.5% | — | — | 0.0% | 2.4% | 31.0% | $10.93 | -20.7% | 1.3 | 67.0% | 21.9% | —x | 14.0x | 2.14 |

|

| TXN | Contender | Texas Instruments Incorporated | Technology | Semiconductors | $283.88 | 2.00% | 2.87% | $1.420 | 4 | $5.680 | $1.420 | Jul 31, 2026 | Aug 11, 2026 | $152.73 | $334.03 | 8.8 | 4.4% | 4.6% | 6.8% | 14.1% | 58.7% | 23.5% | $32.90 | 763.0% | 0.0% | 13.1% | 31.1% | $9.49 | 35.2% | 4.9 | 42.0% | 20.1% | 43.1x | 14.4x | 1.26 |

|

| ENB | Champion | Enbridge Inc | Energy | Oil & Gas Midstream | $54.46 | 3.89% | 6.32% | $0.707 | 3 | $2.121 | $0.712 | Aug 14, 2026 | Sep 1, 2026 | $45.03 | $58.45 | -0.1 | -21.3% | -7.4% | -4.0% | 3.4% | 27.5% | 23.4% | $9.25 | 489.0% | 0.0% | 21.9% | 6.8% | $6.43 | 9.2% | 0.7 | 64.0% | 3.6% | 29.4x | 2.9x | 5.32 |

|

| EPD | Champion | Enterprise Products Partners L. | Energy | Oil & Gas Midstream | $38.05 | 5.89% | 7.96% | $0.560 | 4 | $2.240 | $0.550 | Jul 31, 2026 | Aug 14, 2026 | $30.01 | $40.17 | 10.1 | 3.0% | 4.1% | 4.2% | 3.5% | 39.4% | 22.8% | $14.45 | 163.0% | 0.0% | -6.4% | 10.8% | $0.00 | — | — | — | 10.3% | 13.2x | 2.8x | 1.55 |

|

| VZ | Contender | Verizon Communications Inc. | Communication Services | Telecom Services | $46.81 | 6.05% | 7.09% | $0.708 | 4 | $2.832 | $0.708 | Jul 10, 2026 | Aug 3, 2026 | $38.39 | $51.68 | 8.2 | 3.1% | 2.3% | 2.2% | 2.2% | 23.6% | 22.4% | $19.20 | 144.0% | 0.0% | 2.5% | 11.6% | $9.29 | 15.8% | 0.6 | — | 6.3% | 12.2x | 1.9x | 0.89 |

|

| AMGN | Contender | Amgen Inc. | Healthcare | Drug Manufacturers – General | $411.87 | 2.45% | 3.02% | $2.520 | 4 | $10.080 | $2.520 | Aug 21, 2026 | Sep 11, 2026 | $269.77 | $418.40 | 10.3 | 5.8% | 6.4% | 7.8% | 10.6% | 50.7% | 20.8% | $80.55 | 411.0% | 0.0% | 10.0% | 21.0% | $23.06 | 91.5% | 1.4 | 82.0% | 12.7% | 25.6x | 19.1x | 2.16 |

|

| COST | Contender | Costco Wholesale Corporation | Consumer Defensive | Discount Stores | $944.66 | 0.62% | 1.16% | $1.470 | 4 | $5.880 | $1.470 | Jul 24, 2026 | Aug 7, 2026 | $844.06 | $1,096.50 | -15.0 | 12.6% | 25.2% | -15.7% | 10.2% | -2.6% | 20.8% | $99.50 | 849.0% | 0.0% | 8.2% | 3.0% | $33.82 | 29.2% | 1.1 | 20.0% | 22.4% | 47.5x | 25.3x | 4.60 |

|

| IBM | Champion | International Business Machines | Technology | Information Technology Services | $223.65 | 3.02% | 3.73% | $1.690 | 4 | $6.760 | $1.680 | Aug 10, 2026 | Sep 10, 2026 | $199.19 | $332.46 | 4.5 | 0.6% | 0.6% | 1.5% | 2.9% | -5.5% | 20.7% | $56.25 | 298.0% | 0.0% | 7.6% | 15.5% | $15.80 | 34.5% | 0.8 | 63.0% | 11.8% | 19.9x | 6.1x | 2.27 |

|

| CNQ | Contender | Canadian Natural Resources Limi | Energy | Oil & Gas E&P | $47.19 | 1.87% | 4.46% | $0.442 | 2 | $0.884 | $0.455 | Sep 11, 2026 | Oct 2, 2026 | $29.30 | $51.34 | 7.1 | -44.6% | -21.3% | 5.3% | 10.3% | 61.8% | 20.6% | $20.05 | 135.0% | 0.0% | 8.7% | 26.3% | $8.64 | 26.7% | 1.0 | 24.0% | 19.6% | 11.8x | 2.9x | 3.42 |

|

| MAIN | Contender | Main Street Capital Corporation | Financial Services | Asset Management | $54.41 | 5.84% | 8.76% | $0.265 | 12 | $3.180 | $0.300 | Aug 7, 2026 | Sep 15, 2026 | $48.95 | $67.77 | 17.7 | 2.9% | 12.1% | 11.8% | 4.7% | -1.2% | 20.5% | $23.75 | 129.0% | 0.0% | 4.7% | 74.9% | $-1.76 | 14.4% | 0.2 | 45.0% | 8.0% | 11.5x | 1.6x | 1.76 |

|

| AEP | Contender | American Electric Power Company | Utilities | Utilities – Regulated Electric | $123.03 | 3.09% | 3.51% | $0.950 | 4 | $3.800 | $0.950 | May 8, 2026 | Sep 10, 2026 | $105.70 | $140.58 | 2.3 | -23.4% | -5.0% | -0.8% | 2.4% | 14.5% | 19.7% | $28.85 | 326.0% | 0.0% | 10.9% | 13.8% | $14.13 | 10.1% | 0.5 | 60.0% | 4.0% | 21.3x | 2.1x | 2.14 |

|

| CSX | Contender | CSX Corporation | Industrials | Railroads | $50.31 | 1.11% | 1.28% | $0.140 | 4 | $0.560 | $0.140 | May 29, 2026 | Sep 15, 2026 | $31.80 | $53.60 | 9.6 | 8.0% | 8.7% | 8.4% | 8.4% | 45.5% | 19.7% | $8.60 | 485.0% | 0.0% | -3.1% | 22.2% | $2.87 | 24.4% | 0.8 | 56.0% | 10.1% | 29.3x | 6.6x | 2.04 |

|

| AMP | Contender | Ameriprise Financial, Inc. | Financial Services | Asset Management | $558.43 | 1.22% | 1.42% | $1.700 | 4 | $6.800 | $1.700 | Aug 3, 2026 | Aug 21, 2026 | $422.37 | $565.05 | 10.0 | 7.1% | 8.3% | 8.7% | 8.8% | 13.4% | 19.7% | $20.70 | 2,598.0% | 0.0% | 7.1% | 20.4% | $93.03 | 63.4% | 2.2 | 50.0% | 32.3% | 134.9x | 7.8x | 1.77 |

|

| JNJ | King | Johnson & Johnson | Healthcare | Drug Manufacturers – General | $256.35 | 2.09% | 2.72% | $1.340 | 4 | $5.360 | $1.300 | Aug 25, 2026 | Sep 8, 2026 | $166.64 | $274.90 | 7.2 | 4.4% | 4.6% | 5.1% | 5.6% | 60.2% | 18.7% | $43.05 | 495.0% | 0.0% | 6.1% | 21.5% | $11.46 | 25.7% | 1.1 | 31.0% | 17.5% | 29.8x | 7.3x | 4.23 |

|

| XOM | Champion | ExxonMobil Holdings Corporation | Energy | Oil & Gas Integrated | $155.44 | 2.65% | 3.34% | $1.030 | 4 | $4.120 | $1.030 | May 15, 2026 | Sep 10, 2026 | $105.53 | $176.41 | 5.9 | 4.1% | 4.2% | 3.2% | 3.3% | 50.1% | 18.1% | $29.70 | 423.0% | 0.0% | -5.0% | 8.9% | $16.15 | 12.6% | 1.1 | 12.0% | 11.2% | 26.2x | 2.5x | 1.32 |

|

| AAPL | Contender | Apple Inc. | Technology | Consumer Electronics | $308.91 | 0.35% | 0.45% | $0.270 | 4 | $1.080 | $0.260 | Aug 10, 2026 | Aug 13, 2026 | $201.68 | $344.57 | 5.0 | 4.0% | 4.1% | 4.7% | 7.0% | 53.8% | 18.0% | $43.55 | 609.0% | 0.0% | 6.4% | 27.6% | $9.99 | 148.8% | 1.0 | 40.0% | 76.2% | 35.5x | 42.0x | 2.46 |

|

| KO | King | Coca-Cola Company (The) | Consumer Defensive | Beverages – Non-Alcoholic | $87.05 | 2.44% | 2.83% | $0.530 | 4 | $2.120 | $0.530 | Sep 15, 2026 | Oct 1, 2026 | $65.35 | $90.92 | 7.0 | 4.5% | 4.9% | 4.6% | 4.3% | 30.3% | 16.9% | $16.65 | 423.0% | 0.0% | 2.5% | 28.6% | $3.80 | 42.1% | 1.3 | 51.0% | 19.4% | 26.1x | 10.4x | 4.19 |

|

| QCOM | Contender | QUALCOMM Incorporated | Technology | Semiconductors | $166.44 | 2.21% | 2.06% | $0.920 | 4 | $3.680 | $0.890 | Sep 3, 2026 | Sep 24, 2026 | $121.99 | $259.92 | 8.6 | 4.4% | 5.6% | 6.4% | 6.2% | 17.7% | 16.2% | $218.75 | -24.0% | 0.0% | 13.3% | 21.0% | $11.81 | 33.8% | 2.0 | 32.0% | 23.7% | 19.0x | 6.4x | 0.72 |

|

| PRU | Contender | Prudential Financial, Inc. | Financial Services | Insurance – Life | $121.90 | 4.59% | 4.95% | $1.400 | 4 | $5.600 | $1.400 | May 26, 2026 | Jun 11, 2026 | $91.89 | $127.72 | 8.7 | 3.8% | 3.9% | 4.1% | 7.5% | 30.0% | 16.0% | $55.10 | 121.0% | 0.0% | -15.3% | 6.5% | $31.79 | 12.0% | 0.8 | 43.0% | 7.3% | 11.1x | 1.3x | 1.32 |

|

| FANG | Challenger | Diamondback Energy, Inc. | Energy | Oil & Gas E&P | $202.95 | 2.17% | 4.49% | $1.100 | 4 | $4.400 | $1.050 | May 14, 2026 | May 21, 2026 | $134.30 | $214.51 | 23.9 | -20.8% | -23.0% | 21.8% | — | 45.4% | 15.9% | $4.85 | 4,085.0% | 0.0% | 35.8% | 1.9% | $29.26 | 0.5% | 0.6 | 26.0% | 0.5% | 209.2x | 1.6x | 56.78 |

|

| V | Contender | Visa Inc. | Financial Services | Credit Services | $361.25 | 0.74% | 0.70% | $0.670 | 4 | $2.680 | $0.670 | Aug 11, 2026 | Sep 1, 2026 | $293.89 | $373.97 | 16.3 | 46.9% | 6.1% | 15.6% | 17.0% | 8.9% | 15.7% | $58.75 | 515.0% | 0.0% | 11.3% | 50.8% | $13.25 | 61.2% | 1.0 | 38.0% | 39.7% | 30.7x | 19.1x | 1.64 |

|

| DUK | Contender | Duke Energy Corporation (Holdin | Utilities | Utilities – Regulated Electric | $122.14 | 3.49% | 3.78% | $1.065 | 4 | $4.260 | $1.065 | May 15, 2026 | Sep 16, 2026 | $113.90 | $134.49 | 5.5 | 1.9% | 2.0% | 2.0% | 0.2% | 4.4% | 15.1% | $33.20 | 268.0% | 0.0% | 6.2% | 15.3% | $14.83 | 9.9% | 0.7 | 61.0% | 3.8% | 18.4x | 1.8x | 2.48 |

|

| SO | Contender | Southern Company (The) | Utilities | Utilities – Regulated Electric | $91.52 | 3.32% | 3.52% | $0.760 | 4 | $3.040 | $0.740 | Aug 17, 2026 | Sep 8, 2026 | $83.80 | $100.84 | 6.2 | 2.8% | 2.8% | 2.9% | 3.1% | 3.1% | 14.8% | $20.75 | 341.0% | 0.0% | 10.6% | 15.4% | $9.26 | 11.5% | 0.8 | 64.0% | 4.5% | 22.1x | —x | 2.35 |

|

| WM | Contender | Waste Management, Inc. | Industrials | Waste Management | $227.07 | 1.66% | 1.46% | $0.945 | 4 | $3.780 | $0.945 | Jun 5, 2026 | Jun 18, 2026 | $194.11 | $248.13 | 11.2 | 12.4% | 9.4% | 9.6% | 8.3% | -0.3% | 14.7% | $19.00 | 1,095.0% | 0.0% | 14.2% | 11.1% | $16.30 | 29.8% | 0.9 | 69.0% | 8.9% | 59.8x | 9.2x | 2.33 |

|

| LMT | Contender | Lockheed Martin Corporation | Industrials | Aerospace & Defense | $602.31 | 2.29% | 2.52% | $3.450 | 4 | $13.800 | $3.450 | Sep 1, 2026 | Sep 25, 2026 | $424.12 | $692.00 | 8.3 | 4.6% | 5.0% | 6.0% | 7.8% | 48.6% | 14.0% | $135.50 | 345.0% | 0.0% | 5.6% | 8.2% | $45.07 | 89.2% | 1.2 | 70.0% | 22.6% | 22.2x | 15.8x | 1.22 |

|

| NNN | Champion | NNN REIT, Inc. | Real Estate | REIT – Retail | $47.52 | 5.22% | 5.77% | $0.620 | 4 | $2.480 | $0.600 | Jul 31, 2026 | Aug 14, 2026 | $38.90 | $50.00 | 8.2 | 3.4% | 3.0% | 3.0% | 3.2% | 25.7% | 13.8% | $10.25 | 364.0% | 0.0% | 6.6% | 41.4% | $3.42 | 8.9% | 0.2 | 52.0% | 4.3% | 23.2x | 2.1x | 4.79 |

|

| HTGC | Challenger | Hercules Capital, Inc. | Financial Services | Asset Management | $16.42 | 11.45% | 13.23% | $0.470 | 4 | $1.880 | $0.470 | Aug 11, 2026 | Aug 18, 2026 | $13.70 | $19.67 | 17.2 | 3.3% | -1.2% | 5.8% | 4.2% | 7.0% | 13.8% | $10.10 | 63.0% | 0.0% | 7.9% | 67.7% | $0.05 | 17.3% | 0.1 | 51.0% | 8.4% | 8.1x | 1.4x | 0.52 |

|

| MSFT | Contender | Microsoft Corporation | Technology | Software – Infrastructure | $464.72 | 0.78% | 0.76% | $0.910 | 4 | $3.640 | $0.910 | Aug 20, 2026 | Sep 10, 2026 | $349.20 | $553.72 | 11.0 | 9.9% | 10.2% | 10.2% | 9.9% | -9.9% | 13.6% | $89.70 | 418.0% | 0.0% | 17.8% | 40.3% | $24.64 | 34.0% | 1.2 | 10.0% | 29.5% | 25.9x | 7.8x | 1.52 |

|

| BEN | Champion | Franklin Resources, Inc. | Financial Services | Asset Management | $33.86 | 3.90% | 5.08% | $0.330 | 4 | $1.320 | $0.330 | Jun 29, 2026 | Jul 10, 2026 | $21.11 | $34.92 | 7.3 | 3.1% | 3.3% | 3.4% | 6.6% | 54.7% | 13.3% | $7.35 | 361.0% | 0.0% | 3.5% | 4.0% | $0.53 | 7.9% | 5.5 | 56.0% | 1.4% | 23.0x | 1.5x | 0.38 |

|

| MA | Contender | Mastercard Incorporated | Financial Services | Credit Services | $563.30 | 0.62% | 0.57% | $0.870 | 4 | $3.480 | $0.870 | Jul 9, 2026 | Aug 7, 2026 | $464.52 | $601.77 | 15.0 | 14.6% | 15.3% | 14.4% | 16.5% | -0.7% | 13.3% | $90.90 | 520.0% | 0.0% | 16.4% | 46.3% | $20.05 | 241.2% | 1.1 | 80.0% | 62.2% | 31.0x | 88.1x | 1.72 |

|

| CVX | Champion | Chevron Corporation | Energy | Oil & Gas Integrated | $196.83 | 3.62% | 3.93% | $1.780 | 4 | $7.120 | $1.780 | Aug 19, 2026 | Sep 10, 2026 | $146.49 | $214.71 | 9.6 | 4.5% | 6.0% | 6.0% | 5.0% | 40.3% | 13.1% | $51.95 | 279.0% | 0.0% | -6.8% | 9.6% | $22.76 | — | — | — | 9.7% | 18.9x | 2.1x | 0.80 |

|

| ADC | Challenger | Agree Realty Corporation | Real Estate | REIT – Retail | $77.80 | 3.78% | 4.36% | $0.267 | 11 | $2.937 | $0.267 | Jul 31, 2026 | Aug 14, 2026 | $69.56 | $82.08 | 6.9 | 3.6% | 3.1% | 3.1% | 5.3% | 14.5% | 12.8% | $9.30 | 737.0% | 0.0% | 16.4% | 27.9% | $4.45 | 3.7% | 0.3 | 38.0% | 2.3% | 41.8x | 1.5x | 0.13 |

|

| CSL | Champion | Carlisle Companies Incorporated | Industrials | Building Products & Equipment | $383.60 | 1.15% | 1.00% | $1.100 | 4 | $4.400 | $1.100 | May 18, 2026 | Sep 1, 2026 | $293.43 | $432.91 | 17.1 | 10.0% | 13.6% | 15.9% | 13.9% | 7.2% | 12.0% | $88.15 | 335.0% | 0.0% | 0.3% | 14.2% | $25.43 | 39.2% | 2.6 | 64.0% | 15.6% | 21.8x | 9.4x | 1.29 |

|

| ORCL | Contender | Oracle Corporation | Technology | Software – Infrastructure | $149.97 | 1.33% | 1.29% | $0.500 | 4 | $2.000 | $0.500 | Jul 10, 2026 | Jul 24, 2026 | $114.50 | $345.72 | 13.6 | 11.1% | 11.6% | 12.3% | 12.8% | -38.5% | 11.7% | $29.20 | 414.0% | 0.0% | 17.4% | 25.2% | $11.10 | 53.4% | 1.1 | 80.0% | 10.8% | 25.7x | 11.5x | 0.83 |

|

| NEE | Champion | NextEra Energy, Inc. | Utilities | Utilities – Regulated Electric | $86.92 | 2.87% | 2.57% | $0.623 | 4 | $2.492 | $0.623 | Aug 28, 2026 | Sep 15, 2026 | $69.24 | $98.75 | 13.0 | 10.0% | 10.0% | 10.1% | 11.2% | 30.5% | 11.7% | $22.25 | 291.0% | 0.0% | 10.7% | 32.4% | $6.62 | 11.7% | 0.5 | 63.0% | 6.3% | 19.5x | —x | 1.90 |

|

| UNP | Contender | Union Pacific Corporation | Industrials | Railroads | $293.51 | 1.88% | 2.15% | $1.380 | 4 | $5.520 | $1.380 | Aug 31, 2026 | Sep 30, 2026 | $210.84 | $315.99 | 8.6 | 3.0% | 2.0% | 6.8% | 9.6% | 37.6% | 11.6% | $61.70 | 376.0% | 0.0% | 1.1% | 28.9% | $17.28 | 39.7% | 1.0 | 59.0% | 14.8% | 23.8x | 9.0x | 3.24 |

|

| MRK | Contender | Merck & Company, Inc. | Healthcare | Drug Manufacturers – General | $129.55 | 2.62% | 2.92% | $0.850 | 4 | $3.400 | $0.850 | Sep 15, 2026 | Oct 7, 2026 | $77.58 | $135.05 | 9.0 | 5.0% | 5.3% | 6.3% | 6.8% | 70.2% | 11.4% | $6.25 | 1,973.0% | 0.0% | 1.3% | 4.8% | $20.20 | 7.0% | 1.3 | — | 3.5% | 103.6x | 7.0x | 12.30 |

|

| O | Champion | Realty Income Corporation | Real Estate | REIT – Retail | $63.87 | 5.09% | 5.40% | $0.271 | 12 | $3.252 | $0.271 | Jul 31, 2026 | Aug 14, 2026 | $55.86 | $67.94 | 8.6 | 1.5% | 2.4% | 3.5% | 3.6% | 25.1% | 10.5% | $6.10 | 947.0% | 0.0% | — | 18.9% | — | 2.8% | 2.1 | 42.0% | — | 52.4x | 1.5x | 3.03 |

|

| FRT | King | Federal Realty Investment Trust | Real Estate | REIT – Retail | $116.93 | 3.87% | 4.26% | $1.130 | 4 | $4.520 | $1.130 | Oct 1, 2026 | Oct 15, 2026 | $90.03 | $128.21 | 5.2 | 2.7% | 1.5% | 1.3% | 1.9% | 38.8% | 10.3% | $24.75 | 372.0% | 0.0% | 6.4% | 32.1% | $7.26 | 12.6% | 0.6 | 60.0% | 5.3% | 23.6x | 3.2x | 3.59 |

|

| PLD | Contender | Prologis, Inc. | Real Estate | REIT – Industrial | $137.37 | 3.12% | 2.89% | $1.070 | 4 | $4.280 | $1.070 | Jun 16, 2026 | Jun 30, 2026 | $103.41 | $153.35 | 14.6 | 5.6% | 7.8% | 11.4% | 9.8% | 38.3% | 8.4% | $22.45 | 512.0% | 0.0% | — | 43.6% | $5.51 | 7.8% | 0.7 | 40.0% | — | 30.6x | 2.4x | 129.33 |

|

| BMY | Contender | Bristol-Myers Squibb Company | Healthcare | Drug Manufacturers – General | $64.71 | 3.89% | 4.31% | $0.630 | 4 | $2.520 | $0.630 | Jul 2, 2026 | Aug 3, 2026 | $42.52 | $68.10 | 9.4 | 2.0% | 3.7% | 5.5% | 5.2% | 53.3% | 8.1% | $113.50 | -43.0% | 0.0% | -0.2% | 18.9% | $6.26 | 46.6% | 1.5 | 66.0% | 14.4% | 14.3x | 5.9x | 2.29 |

|

| KR | Contender | Kroger Company (The) | Consumer Defensive | Grocery Stores | $56.57 | 2.47% | 2.02% | $0.350 | 4 | $1.400 | $0.350 | May 15, 2026 | Sep 1, 2026 | $54.15 | $76.58 | 16.7 | 9.4% | 10.4% | 14.2% | 12.8% | -20.3% | 8.1% | $42.75 | 32.0% | 0.0% | — | 0.7% | — | 13.8% | 0.8 | 77.0% | — | 33.1x | 6.1x | 0.55 |

|

| TGT | King | Target Corporation | Consumer Defensive | Discount Stores | $144.49 | 3.16% | 3.08% | $1.140 | 4 | $4.560 | $1.140 | Aug 12, 2026 | Sep 1, 2026 | $83.44 | $147.77 | 14.0 | 1.8% | 1.8% | 10.9% | 7.4% | 55.9% | 7.9% | $37.85 | 282.0% | 0.0% | — | 3.2% | — | 22.0% | 0.9 | 52.0% | — | 19.1x | 4.0x | 2.68 |

|

| STAG | Contender | Stag Industrial, Inc. | Real Estate | REIT – Industrial | $36.67 | 11.64% | 4.08% | $0.388 | 11 | $4.268 | $0.388 | Sep 30, 2026 | Oct 15, 2026 | $34.18 | $42.61 | 10.9 | -5.9% | -1.7% | -0.7% | 0.1% | 14.1% | 6.4% | $6.50 | 464.0% | 0.0% | 10.1% | 28.0% | $2.47 | 7.0% | 1.8 | 45.0% | 3.8% | 28.2x | 2.0x | 19.49 |

|

| ADP | King | Automatic Data Processing, Inc. | Technology | Software – Application | $270.33 | 2.52% | 2.11% | $1.700 | 4 | $6.800 | $1.700 | Sep 11, 2026 | Oct 1, 2026 | $188.16 | $310.08 | 14.9 | 10.3% | 11.5% | 12.4% | 12.3% | -6.9% | 5.9% | $54.65 | 395.0% | 0.0% | 6.7% | 20.1% | $13.70 | 72.2% | 1.1 | 47.0% | 40.7% | 24.7x | 17.8x | 2.54 |

|

| IIPR | Challenger | Innovative Industrial Propertie | Real Estate | REIT – Industrial | $58.81 | 9.69% | 10.62% | $1.900 | 3 | $5.700 | $1.900 | Jun 30, 2026 | Jul 15, 2026 | $44.58 | $65.38 | 17.9 | 0.0% | 1.8% | 8.2% | — | 49.1% | 5.8% | $19.60 | 200.0% | 0.0% | -13.8% | 43.4% | $6.90 | 6.3% | 0.4 | 14.0% | 5.4% | 15.0x | 0.9x | 1.26 |

|

| COP | Challenger | ConocoPhillips | Energy | Oil & Gas E&P | $120.48 | 2.79% | 3.45% | $0.840 | 4 | $3.360 | $0.840 | May 11, 2026 | Jun 1, 2026 | $85.57 | $135.87 | 16.7 | 5.8% | -14.6% | 13.9% | 8.3% | 37.9% | 5.6% | $29.50 | 308.0% | 0.0% | 8.1% | 12.1% | $14.76 | 11.3% | 1.3 | 26.0% | 8.4% | 20.4x | 2.3x | 1.02 |

|

| HD | Contender | Home Depot, Inc. (The) | Consumer Cyclical | Home Improvement Retail | $349.77 | 2.66% | 2.44% | $2.330 | 4 | $9.320 | $2.330 | Jun 4, 2026 | Jun 18, 2026 | $289.10 | $426.75 | 10.7 | 1.8% | 5.1% | 8.0% | 13.7% | -5.0% | 5.6% | $70.40 | 397.0% | 0.0% | — | 8.4% | — | 128.4% | 1.1 | 79.0% | — | 24.8x | 25.1x | 2.01 |

|

| TROW | Champion | T. Rowe Price Group, Inc. | Financial Services | Asset Management | $111.75 | 4.65% | 4.59% | $1.300 | 4 | $5.200 | $1.300 | Jun 15, 2026 | Jun 29, 2026 | $85.22 | $122.00 | -1.2 | 2.4% | 2.0% | -5.9% | 9.3% | 19.4% | 4.9% | $49.80 | 124.0% | 0.0% | 4.1% | 28.4% | $9.02 | 19.4% | 4.0 | — | 19.3% | 11.2x | 2.2x | 6.39 |

|

| MDT | Champion | Medtronic plc. | Healthcare | Medical Devices | $85.39 | 3.37% | 3.12% | $0.720 | 4 | $2.880 | $0.710 | Jun 26, 2026 | Jul 17, 2026 | $73.31 | $106.33 | 7.1 | 1.4% | 1.4% | 3.8% | 6.1% | 2.0% | 4.8% | $18.65 | 358.0% | 0.0% | — | 13.2% | — | 9.8% | 2.1 | 35.0% | — | 22.9x | 2.2x | 1.69 |

|

| SBUX | Contender | Starbucks Corporation | Consumer Cyclical | Restaurants | $105.39 | 2.35% | 2.28% | $0.620 | 4 | $2.480 | $0.620 | Aug 14, 2026 | Aug 28, 2026 | $77.99 | $109.23 | 15.2 | 2.9% | -1.8% | 12.8% | 11.9% | 20.2% | 4.4% | $43.25 | 144.0% | 0.0% | 2.8% | 5.2% | $4.37 | — | 0.8 | 1.6% | 14.6% | 60.9x | —x | 1.28 |

|

| ABT | Contender | Abbott Laboratories | Healthcare | Medical Devices | $108.93 | 2.31% | 1.95% | $0.630 | 4 | $2.520 | $0.630 | Jul 15, 2026 | Aug 17, 2026 | $81.97 | $137.49 | 10.0 | 6.9% | 7.4% | 7.7% | 9.3% | -15.1% | 4.2% | $15.45 | 605.0% | 0.0% | — | 11.7% | $5.72 | 10.6% | 1.4 | — | — | 35.3x | 3.7x | 2.17 |

|

| IEX | Contender | IDEX Corporation | Industrials | Specialty Industrial Machinery | $234.21 | 1.25% | 1.27% | $0.730 | 4 | $2.920 | $0.730 | Jul 6, 2026 | Jul 24, 2026 | $157.25 | $243.80 | 8.0 | 2.9% | 5.1% | 6.7% | 8.1% | 52.0% | 3.7% | $34.70 | 575.0% | 0.0% | 5.8% | 14.5% | $9.72 | 13.0% | 3.1 | 32.0% | 8.8% | 33.8x | 4.3x | 1.95 |

|

| SWK | King | Stanley Black & Decker, Inc. | Industrials | Tools & Accessories | $94.58 | 3.51% | 3.67% | $0.830 | 4 | $3.320 | $0.830 | Sep 8, 2026 | Sep 22, 2026 | $61.90 | $96.04 | 7.0 | 1.2% | 1.2% | 3.5% | 4.2% | 52.8% | 3.7% | $102.25 | -8.0% | 0.0% | -1.5% | 4.1% | $10.27 | 6.9% | 1.4 | 34.0% | 4.5% | 23.1x | 1.6x | 1.39 |

|

| HPQ | Contender | HP Inc. | Technology | Computer Hardware | $30.25 | 3.97% | 3.73% | $0.300 | 4 | $1.200 | $0.300 | Sep 9, 2026 | Oct 7, 2026 | $17.56 | $30.87 | 13.4 | 4.0% | 4.6% | 9.4% | 10.2% | 26.6% | 2.5% | $13.50 | 124.0% | 0.0% | — | 4.5% | — | — | 0.8 | 1.0% | — | 11.2x | —x | 24.71 |

|

| VICI | Challenger | VICI Properties Inc. | Real Estate | REIT – Diversified | $26.35 | 6.83% | 5.59% | $0.450 | 4 | $1.800 | $0.450 | Jun 18, 2026 | Jul 9, 2026 | $25.82 | $34.01 | 13.2 | 3.9% | 4.9% | 6.4% | — | -9.5% | 2.5% | $12.90 | 104.0% | 0.0% | 4.1% | 67.5% | $2.40 | 9.9% | 11.2 | 38.0% | 6.0% | 10.2x | 1.0x | — |

|

| ADM | King | Archer-Daniels-Midland Company | Consumer Defensive | Farm Products | $79.27 | 2.62% | 2.76% | $0.520 | 4 | $2.080 | $0.520 | May 20, 2026 | Jun 10, 2026 | $53.56 | $88.46 | 9.8 | 2.0% | 6.6% | 7.1% | 5.9% | 55.8% | 1.9% | $11.20 | 608.0% | 0.0% | — | 1.3% | — | 4.8% | 1.3 | 25.0% | — | 35.4x | 1.7x | 2.40 |

|

| AMT | Contender | American Tower Corporation (REI | Real Estate | REIT – Specialty | $169.95 | 4.21% | 3.14% | $1.790 | 4 | $7.160 | $1.790 | Jun 12, 2026 | Jul 13, 2026 | $160.06 | $214.79 | 11.7 | 5.1% | 4.3% | 7.5% | 13.4% | -11.0% | 1.7% | $30.95 | 449.0% | 0.0% | 5.1% | 31.1% | $12.39 | 33.9% | 0.4 | 92.0% | 7.6% | 27.5x | 21.3x | 1.61 |

|

| MCD | King | McDonald's Corporation | Consumer Cyclical | Restaurants | $272.79 | 2.73% | 2.19% | $1.860 | 4 | $7.440 | $1.860 | Sep 1, 2026 | Sep 16, 2026 | $260.96 | $341.75 | 10.2 | 5.3% | 7.4% | 7.5% | 7.6% | -6.1% | 1.5% | $61.50 | 344.0% | 0.0% | 3.7% | 31.6% | $16.41 | — | 1.1 | — | 16.7% | 22.2x | —x | 2.55 |

|

| PG | King | Procter & Gamble Company (The) | Consumer Defensive | Household & Personal Products | $144.49 | 3.01% | 2.59% | $1.089 | 4 | $4.356 | $1.089 | Jul 24, 2026 | Aug 17, 2026 | $137.62 | $167.25 | 8.3 | 4.0% | 5.0% | 5.3% | 4.9% | 1.7% | 0.8% | $33.10 | 337.0% | 0.0% | 3.3% | 18.4% | $8.40 | 30.3% | 0.7 | — | 20.8% | 21.8x | 6.3x | 5.57 |

|

| DVN | Challenger | Devon Energy Corporation | Energy | Oil & Gas E&P | $45.13 | 2.84% | 4.72% | $0.320 | 4 | $1.280 | $0.240 | Jun 15, 2026 | Jun 30, 2026 | $31.47 | $52.71 | 1.4 | -8.8% | -38.7% | -1.5% | 2.9% | 47.4% | 0.2% | $17.95 | 151.0% | 0.0% | — | 14.2% | — | 15.2% | 1.0 | 33.0% | — | 12.6x | 1.8x | 2.92 |

|

| KMB | King | Kimberly-Clark Corporation | Consumer Defensive | Household & Personal Products | $109.31 | 4.68% | 3.78% | $1.280 | 4 | $5.120 | $1.280 | Jun 5, 2026 | Jul 2, 2026 | $92.42 | $137.46 | 7.5 | 2.4% | 2.8% | 2.8% | 3.5% | -8.2% | 0.1% | $25.85 | 323.0% | 0.0% | -18.0% | 12.8% | $9.63 | 111.7% | 0.8 | 78.0% | 26.7% | 21.1x | 20.2x | 2.21 |

|

| MDLZ | Contender | Mondelez International, Inc. | Consumer Defensive | Confectioners | $61.65 | 2.43% | 2.57% | $0.500 | 3 | $1.500 | $0.500 | Jun 30, 2026 | Jul 14, 2026 | $51.20 | $66.65 | 12.1 | 6.4% | 9.1% | 9.7% | 11.4% | 6.5% | -2.0% | $8.15 | 656.0% | 0.0% | 5.8% | 8.9% | $3.48 | 13.3% | 0.6 | — | 8.1% | 37.8x | 3.0x | 1.04 |

|

| PFE | Contender | Pfizer, Inc. | Healthcare | Drug Manufacturers – General | $25.01 | 6.88% | 5.82% | $0.430 | 4 | $1.720 | $0.430 | Jul 24, 2026 | Sep 1, 2026 | $23.40 | $28.75 | 9.2 | 0.6% | 1.8% | 2.4% | 4.6% | 21.8% | -2.5% | $6.55 | 282.0% | 0.0% | — | 11.8% | — | 8.3% | 1.3 | 40.0% | — | 19.1x | 1.6x | 2.94 |

|

| HSY | Contender | The Hershey Company | Consumer Defensive | Confectioners | $182.20 | 3.19% | 2.39% | $1.452 | 4 | $5.808 | $1.452 | May 15, 2026 | Sep 15, 2026 | $161.43 | $239.48 | 15.1 | 3.0% | 10.8% | 11.9% | 9.2% | 5.0% | -2.9% | $182.75 | 0.0% | 0.0% | 4.4% | 12.2% | $18.16 | 32.8% | 1.2 | 52.0% | 15.5% | 24.9x | 8.0x | 1.04 |

|

| AES | Contender | The AES Corporation | Utilities | Utilities – Diversified | $14.73 | 4.78% | 4.26% | $0.176 | 4 | $0.704 | $0.176 | Jul 31, 2026 | Aug 14, 2026 | $12.33 | $17.65 | 8.2 | 0.4% | 2.4% | 3.4% | 5.1% | 23.5% | -3.0% | $15.14 | -3.0% | 0.0% | -0.4% | 4.9% | $7.05 | 9.6% | 0.8 | 85.0% | 2.0% | 5.5x | 2.1x | 0.81 |

|

| UNH | Contender | UnitedHealth Group Incorporated | Healthcare | Healthcare Plans | $410.15 | 2.26% | 1.67% | $2.320 | 4 | $9.280 | $2.210 | Jun 15, 2026 | Jun 23, 2026 | $252.14 | $461.62 | 13.7 | 5.2% | 9.4% | 11.5% | 15.5% | 71.5% | -4.0% | $66.35 | 518.0% | 0.0% | 11.8% | 3.1% | $29.75 | 14.2% | 0.8 | 42.0% | 8.4% | 30.9x | 3.6x | 1.25 |

|

| PEP | King | Pepsico, Inc. | Consumer Defensive | Beverages – Non-Alcoholic | $139.56 | 4.24% | 3.10% | $1.480 | 4 | $5.920 | $1.423 | Sep 4, 2026 | Sep 30, 2026 | $133.73 | $171.48 | 11.0 | 4.8% | 6.8% | 6.8% | 7.2% | 8.5% | -4.8% | $38.15 | 266.0% | 0.0% | 2.3% | 10.8% | $9.85 | 51.5% | 0.9 | 66.0% | 16.4% | 18.3x | 8.6x | 1.51 |

|

| INFY | Challenger | Infosys Limited | Technology | Information Technology Services | $12.03 | 4.31% | 2.75% | $0.259 | 2 | $0.518 | $0.259 | Jun 10, 2026 | Jun 29, 2026 | $10.30 | $30.00 | 11.6 | 2.2% | 7.8% | 7.3% | 10.9% | -20.7% | -5.8% | $4.05 | 197.0% | 0.0% | 9.6% | 16.4% | $1.01 | 32.0% | 1.9 | 6.0% | 2,831.4% | 14.9x | 10.1x | 2.05 |

|

| LYB | Contender | LyondellBasell Industries NV | Basic Materials | Specialty Chemicals | $60.91 | 4.53% | 7.69% | $0.690 | 4 | $2.760 | $0.690 | Jun 1, 2026 | Jun 8, 2026 | $41.58 | $83.94 | 3.8 | -23.6% | -5.1% | -0.8% | 2.6% | 42.8% | -7.6% | $27.70 | 120.0% | 0.0% | -25.2% | -1.1% | $9.20 | -2.3% | 1.6 | 54.0% | -1.5% | —x | 1.8x | 1.53 |

|

| UPS | Contender | United Parcel Service, Inc. | Industrials | Integrated Freight & Logistics | $104.22 | 6.29% | 4.77% | $1.640 | 4 | $6.560 | $1.640 | May 18, 2026 | Jun 4, 2026 | $82.00 | $122.41 | 16.4 | 0.3% | 1.5% | 10.1% | 8.1% | 40.1% | -10.4% | $26.90 | 287.0% | 0.0% | -2.7% | 5.1% | $13.48 | 29.6% | 1.2 | — | 10.6% | 19.4x | 5.9x | 1.63 |

|

| CMCSA | Contender | Comcast Corporation | Communication Services | Telecom Services | $24.97 | 5.29% | 3.40% | $0.330 | 4 | $1.320 | $0.330 | Oct 7, 2026 | Oct 28, 2026 | $21.28 | $32.86 | 12.9 | 8.3% | 7.4% | 7.6% | 10.2% | -7.2% | -12.0% | $15.60 | 60.0% | 0.0% | 0.0% | 9.0% | $9.19 | 11.5% | 0.8 | 48.0% | 6.1% | 8.0x | 1.0x | 142.98 |

|

| ACN | Contender | Accenture plc | Technology | Information Technology Services | $176.58 | 2.77% | 1.65% | $1.630 | 3 | $4.890 | $1.630 | Jul 9, 2026 | Aug 14, 2026 | $118.15 | $291.09 | 1.2 | -44.9% | -10.1% | -1.5% | 4.0% | -23.3% | -15.1% | $62.55 | 182.0% | 0.0% | 7.4% | 10.7% | $21.54 | 24.4% | 1.3 | 19.0% | 20.1% | 14.1x | 3.4x | 1.28 |

|

| GIS | Challenger | General Mills, Inc. | Consumer Defensive | Packaged Foods | $35.75 | 6.83% | 4.07% | $0.610 | 4 | $2.440 | $0.610 | Jul 10, 2026 | Aug 3, 2026 | $31.75 | $51.33 | 10.5 | 1.2% | 3.4% | 3.6% | 3.0% | -17.1% | -16.2% | $17.75 | 101.0% | 0.0% | — | -0.5% | — | -1.0% | 0.7 | 63.0% | — | —x | 3.5x | 11.74 |

|

| NKE | Contender | Nike, Inc. | Consumer Cyclical | Footwear & Accessories | $41.56 | 3.95% | 1.63% | $0.410 | 4 | $1.640 | $0.410 | Jun 1, 2026 | Oct 1, 2026 | $40.00 | $80.17 | 12.7 | 3.8% | 7.1% | 8.8% | 10.1% | -40.2% | -25.0% | $10.50 | 296.0% | 0.0% | 0.2% | 6.7% | $2.39 | 22.1% | 2.0 | 37.0% | 13.1% | 19.8x | 4.2x | 1.55 |

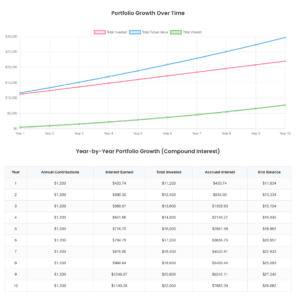

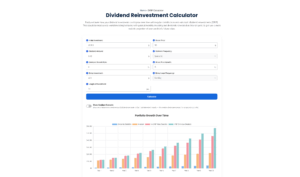

Calculators

Dividend ETF Calculators

Get started with DRIP investing using our calculators. Fill in the information, and it will show you dividend returns.

For beginners

Getting started

Starting with DRIP investing is simple. It’s about making small, regular investments grow over time, just like how Coca-Cola started. Here, we’ll explain the easy steps from your first dividend to picking a DRIP plan that fits you. Let’s get those dividends to build up your savings.

Participating in the DRIP

Generally, there are three ways investors can participate in dividend reinvestment plans: company-run plans, transfer agent plans, and brokerage plans

Company run plans

Many companies run these programs through their investor relations or shareholder services departments. Several companies have even started to offer Individual Retirement Accounts in addition to their reinvestment plans.

Companies may have participation rules that include owning at least one share prior to joining the dividend reinvestment plan. They may also require the stock to be in the investor’s name rather than street name.

A phone call to the shareholder services department is an effective way to learn about company-specific participation rules.

Transfer agent plans

Due to the overwhelming popularity of some DRIPs, companies may engage the help of transfer agents to administer their programs. The transfer agent is a third-party broker that typically runs plans for many different companies.

Since the transfer agent is running multiple programs using the same resources, they can do it more cost-effectively than some of the issuing companies.

Some of the larger transfer agents include American Stock Transfer & Trust Company, Mellon Investor Services, and ComputerShare.

Brokerage plans

While dividend reinvestment programs reduce the fees collected by traditional brokerage houses, many of these firms now attempt to mirror DRIPs by offering the ability to reinvest dividends without charging a fee.

Unfortunately, these plans usually lack the most attractive feature of a real DRIP: The cash purchase of new shares of stock without fees.

More on DRIP brokersStrategies

Dividend investing strategies

Learn about Dividend Investing Strategies in a way that’s easy to understand. This section will show you how to pick good stocks that pay dividends and make a plan to earn regular income from them. Get ready to grow your money smarter.

dividend champions

Future dividend champions

Meet the Future Dividend Champions. These companies are on track to becoming top picks for investors who love getting regular dividend payments. In this section, we’ll show you why these stocks stand out and how they could help give your investments a boost over time. Start exploring which one might be the champion for your portfolio.

3000+

Downloads

20+

Years in drip investing

stay updated

Dividend champions spreadsheet

Dividend champions are companies that have consistently raised their dividends each year for multiple years in a row.

Use our Dividend Champions spreadsheet for the latest list of dividend champions, contenders, and challengers.

Updated monthly on the 1st.

Download nowresources & tools

Resources for the dividend investor

Fill your investor’s toolbox with our handpicked list of easy-to-read books. If you’re just starting or already know a lot about investing, these books are full of tips and advice to help you make money with dividends. Check out our favorites and learn new ways to improve your investments.

For experts

Deep dive into drip investing

Dive into the world of dividend reinvestment. Find out how to pick stocks that can grow your money and learn easy ways to save on taxes. These articles will help you understand how to make smart choices for building your investments over time.

NEWS

Recent Dividend News

Stay in the know with our dividend and DRIP news. We cover everything from stock predictions, to company performance, investment insights, ETFs and more.

as seen on

DripInvesting on the web

“THANK YOU SO MUCH FOR THIS.

How the heck did i not know this existed?!

A huge thank you to the creator(s) and editor(s) of this document!”

u/LordGuardial

“This is awesome!

I started with dripinvesting.org when I first started really focusing on dividends.

Thank you for sharing.”

u/pinetree64