DRIP Investing: Getting Started

Starting with DRIP investing is simple. It's about making small, regular investments grow over time, just like how Coca-Cola started. Here, we'll explain the easy steps from your first dividend to picking a DRIP plan that fits you. Let's get those dividends to build up your savings.

Dividend Investing Strategies

Learn about Dividend Investing Strategies in a way that's easy to understand. This section will show you how to pick good stocks that pay dividends and make a plan to earn regular income from them. Get ready to grow your money smarter.

Future Dividend Champions

Meet the Future Dividend Champions. These companies are on track to becoming top picks for investors who love getting regular dividend payments. In this section, we'll show you why these stocks stand out and how they could help give your investments a boost over time. Start exploring which one might be the champion for your portfolio.

Resources for the Dividend Investor

Fill your investor's toolbox with our handpicked list of easy-to-read books. If you're just starting or already know a lot about investing, these books are full of tips and advice to help you make money with dividends. Check out our favorites and learn new ways to improve your investments.

Deep Dive into Drip Investing

Dive into the world of dividend reinvestment. Find out how to pick stocks that can grow your money and learn easy ways to save on taxes. These articles will help you understand how to make smart choices for building your investments over time.

DRIP Investing (Dividend Reinvestment Plans)

The term DRIP is an abbreviation for dividend reinvestment plans, which offer investors the opportunity to reinvest all, or a portion, of their dividend payments back into a company's stock. Oftentimes, companies will allow investors to purchase additional shares of stock through these programs too.

What is DRIP Investing?

Dividend reinvestment plans are sponsored by companies that allow individual investors to purchase common stock without going through a broker. The name comes from the plan's policy of allowing the investor to automatically reinvest dividends to purchase additional shares of stock.

Many DRIPs are offered to investors free of any participation costs, while others charge relatively small administration fees or commissions. While the name implies these plans are limited to reinvesting stock dividends, some plans allow participants to directly purchase a company's stock. This enhanced practice is sometimes referred to as optional cash purchases or OCPs.

Advantages

A large number of companies offer dividend reinvestment programs, and participation rules are usually outlined in the investor section of the company's website. Since these plans are flexible enough to allow even small purchases without a broker's fee, it's hard to find any downside to these offerings. In fact, there are several significant advantages of these programs including:

Low Cost of Entry: investors don't need a lot of money to enroll in these programs, most companies allow the purchase of just a single share of stock, and often this purchase is at a discount.

Cost Effective: since the investor isn't paying brokerage fees, all of the money is put to work. Over 100 companies allow investors to purchase stock at a discount to the current market price through optional cash purchase plans, or OCPs.

Dollar Cost Averaging: finally, many of the DRIPs allow investors to purchase stock through automated weekly or monthly deductions. This long-term purchase strategy provides the investor with a less painful, and more structured, approach to buying stocks.

Participation

Generally, there are three ways investors can participate in dividend reinvestment plans:

Company Run Plans

Transfer Agent Plans

Brokerage Plans

Company Run Plans

Many companies run these programs through their investor relations or shareholder services departments. Several companies have even started to offer Individual Retirement Accounts in addition to their reinvestment plans. Companies may have participation rules that include owning at least one share prior to joining the dividend reinvestment plan. They may also require the stock to be in the investor's name rather than street name. A phone call to the shareholder services department is an effective way to learn about company-specific participation rules.

Transfer Agent Plans

Due to the overwhelming popularity of some DRIPs, companies may engage the help of transfer agents to administer their programs. The transfer agent is a third party broker that typically runs plans for many different companies. Since the transfer agent is running multiple programs using the same resources, they can do it more cost-effectively than some of the issuing companies.

Some of the larger transfer agents include American Stock Transfer & Trust Company, Mellon Investor Services, and ComputerShare.

Brokerage Plans

While dividend reinvestment programs reduce the fees collected by traditional brokerage houses, many of these firms now attempt to mirror DRIPs by offering the ability to reinvest dividends without charging a fee. Unfortunately, these plans usually lack the most attractive feature of a real DRIP: The cash purchase of new shares of stock without fees.

How Many Stocks Should You Own?

A reader asked me a question that boiled down to them wanting to know how many stocks should be in their portfolio. It is a question with an answer that will be different for each person, but knowing how to arrive at that answer is simple.

Many people own more companies than I do. This is a personal choice, so if that number works for them, then it is the correct number. As a serious photographer who works with historical processes, I have always said that whatever means one chooses to share their vision, if it is successful for them to do so, then that is the correct choice. As noted in a previous article, I feel that this is the same with investing.

Figuring This Out

Initially, my approach to selecting companies was haphazard. Upon seeing a company that I thought would do well in the short run, I would buy it – simple as that. It led to numerous trades, which worked well, until it did not work well. In the late 1990s, most of us were geniuses, and in the early 2000s, most of us were idiots. (The uninitiated can look at the DOW’s price change during those periods.)

Reexamining my investment philosophy, I decided to examine what had worked for me and what had not. One of the many lessons learned from the early 2000s was that I had owned too many companies. To remedy this, I took an example from one of my hobbies – numismatics.

I started collecting coins when I was around 7 or 8 years old. Pennies were the only thing I could afford to collect (even in the late 1950s, 25 cents a week allowance was not much). As time went on, I could afford to invest more into my hobby and expanded to other denominations, and eventually ended up all over the place. I finally decided that it was time to specialize.

Specialization led me to 18th-century British tokens, with which I had grown a fond interest, as each token had a real story. Even this was too wide, so I narrowed things down to collect only tokens in R. C. Bell’s book, Commercial Coins. I now have a focused collection of interesting tokens over two hundred years old. Yes, I still have most of my other coins, but I am most proud of the token collection.

Back to Investing

Through the years that led up to the early 2000s, it was dividend companies and my participation in DRiPs that had been steadfast. I had “collected” dividend companies that looked good, and in turn, good things had happened.

The issue was that I had so many companies that I felt like I was in a boat without a paddle. I was going in the right direction but would not be able to maneuver if an obstacle got in the way.

As in chess (another hobby of mine), it was time to figure out how I wanted the board to look, and then work to make it so. I decided to trim the number of companies I owned to the point where I could track them.

Finally, the Answer

How many dividend companies should one own? One should own only as many companies as one can track. Owning companies that are not within the understanding and/or view of the owner moves toward speculation – one simply hopes that things will work out in the end.

What do I mean by "track?" You track a company by knowing what the company is doing, and you know what a company is doing, in the least, by scanning the quarterly and annual reports. These reports can be scanned because you are looking for specific things explained within.

It goes back to a suggestion I made long ago that one should write down (or type into a document) the reasons for buying a company before making the purchase. By physically committing the decision to paper or an electronic document, the reasoning is real, and ensures that there is more to the decision than, "I think it will make me money."

The information within the quarterly and annual reports should support those reasons. If they are not supported, then the company should be flagged for further study. Was my initial assessment incorrect? Do I understand the reason for the change? Is this a temporary setback, or is it a change in the company's direction?

An extreme example was my purchase of Enron. When I started buying shares, the company was the largest supplier of natural gas in North America, which was the reason I selected it. They had solid earnings (until they didn't and lied about it) and fulfilled my reason for purchase. We all know what happened later.

The red flag came when the company changed its focus to something completely outside of its core competency. I hung on for a short while, hoping that this would work itself out, but soon realized that something was seriously wrong and sold my shares. Of course, this is a mere thumbnail of what happened but is instructive. One cannot buy and hope, one needs to buy and understand.

A more concrete example for me is National Fuel Gas. I have made several purchases because I see the company’s ability to grow. For instance, they intend to expand their interstate pipeline system through several projects currently underway. It only takes a moment to check the progress of this in their 10-Q report.

I urge readers not to jump to the conclusion of selling if a milestone is not reached. Especially now, with COVID still creating havoc, there are many legitimate reasons a company may not be able to deliver. One needs to understand if the situation is a temporary setback or a permanent one, which could be the difference between holding and selling.

Also, though a company's direction may be changed, this should not necessarily be the death knell for holding the stock. Changing circumstances require consideration, but if we are not keeping track of the company in the first place, then the point is moot.

In addition to what the company is doing, I like to keep track of the ex-div dates. It does happen that occasionally I come across some extra cash. The question then becomes how it will be invested, and I always want to select the best company available. As often as not, however, several current holdings look good to me.

A company with an ex-div date on the horizon will often serve as a good tie-breaker. It allows me to grab a small advantage when it comes to getting a return on my investment. I used to keep a list of such dates in my spreadsheet, but that required manual entry, which was less than convenient. Fortunately, Stock Rover has this information easily at hand.

Chart available via Stock Rover

Another reason for keeping track of the ex-div date is that when it is established, not only the date of the next dividend is known, but also the amount. A company that cuts its dividend is a sell signal for me, so I want to know if/when it happens.

Finishing Up

I have mentioned photography, numismatics, and chess as hobbies in this article and could continue with music composition, reading, travel, writing stories for my granddaughter, and so on. I have a host of things outside of investing where I want to spend my time, so for me, a dozen companies appears to be the sweet spot of having enough companies in which to invest, and not so many that it takes away from the other things I want to do.

This way, I can spend a couple of hours a week tracking the companies I own, writing articles for this blog, and considering new investments if the need arises, and still have time to spend on my many other interests.

I have friends who spend more time with their investments, so creating their own mutual fund works for them. I own a couple of index funds for diversification, so I do not see this need for myself. However, if this works for others, then it is the right decision for them.

So my advice is not to own more stocks than you can afford to follow, and that number can range between just a few to a hundred or more (yes, I know people who own that many). There is no right or wrong number, as long as that number works well for you.

Are Dividend Reinvestment Programs Dead?

Dividend Reinvestment Programs have been a staple for acquiring shares for years. An alternative that supersedes this option is holding shares through a broker that offers the same advantages. It is instructive to evaluate this option to determine if this DRiP still has a place for the dividend investor.

A question that has been asked on numerous message boards is whether or not the idea of dividend reinvestment programs is dead. While there are gradations of nuance within the question itself, the answer is that yes, they are dead. The idea, itself, is solid for dividend investors, but the execution is lacking.

I will expand on this to assure the reader of the exact reasons for my opinion.

Dividend reinvestment programs go back many years. My grandfather was an engineer for AT&T. I am not sure of the exact years, but probably from about 1925-1965. AT&T, as well as numerous other companies, encouraged their employees to purchase stock in their company, and made it easy for them to do so.

There were many reasons for this, but one of the best was to give employees some "skin in the game." If the company did well, then the shareholders did well. Employee shareholders had added incentive to perform their best for the good of the company.

My grandfather participated in AT&T's dividend reinvestment program, and when he passed away, my mother got half of the stock that had accumulated. My parents used that money to build a house that my father designed (he was an architect). This was an excellent example of the strength of setting a little aside regularly over a long period of time.

Comsat check somewhat participated in one 35 years ago. When I worked for Comsat, one of my benefits was to receive stock in the company. At the time, I knew nothing about investing and was a little confused when I would occasionally receive a check for a pocketful of change. Eventually, the company laid off a bunch of us and I stopped receiving those mystery checks.

I began earnestly investing in the early 1990s, and upon reading an article in The Motley Fool about DRiPs, I became immersed with the idea. It made so much sense to make small purchases regularly. I saw what my grandfather had accomplished and decided to go that route.

This resulted in becoming a weekly author for the website. When Internet companies fell apart in 2000, they purged the paid authors on the website, the company decided to charge admission to their message boards, and I started writing my own drip investing advice.

This is a long explanation to show that I appreciate the strength of dividend reinvestment programs and stress the importance they have had in my life, as they were instrumental in allowing me to retire years seven years before taking Social Security. But like any tool, despite its success in the past, its continued use constantly needs to be reassessed.

Today there are advantages to using a discount broker instead of starting a traditional DRiP. To successfully do so, the broker must have the ability to offer the two things that make DRiPs so attractive.

Make fee-free purchases

Automatically reinvest dividends

I will look at these one at a time.

Make fee-free purchases

My grandfather did not have to pay a fee to make AT&T stock purchases through the company. Over 20 years ago, when I found an interest in DRiPs, many companies allowed share purchases without cost. As the popularity of these programs increased, many of these companies decided to charge for purchases.

These fees came not only in the form of purchases of new shares but sometimes even in the purchase of shares through dividend reinvestment! When I first started to see this happen, it was hard to believe. Even my beloved Coke, a company created by a distant relative, Asa Griggs Candler, and one that I had held for many years, attending numerous annual meetings (and meeting Warren Buffet), began to charge such fees.

For years, I wrote about the many quality companies that offered fee-free DRiPs and pointed people to MoneyPaper (now directinvesting.com). Now I see the company offers enrollments for only 55 fee-free DRiPs. The trend has become painfully obvious.

Numerous discount brokers allow the purchase of equities without cost. When I started investing in 1992, purchasing stock (if I remember correctly) cost $29.95 at Schwab. I remember going to their office in Annapolis twice to make purchases. Now purchasing through them is free. I use Ally, but TD Ameritrade, Fidelity, and many others offer the same thing.

Automatically reinvest dividends

It happens regularly when I get an email from Ally letting me know that I have received a dividend. It is a real pleasure to log into my account to see how many additional shares have been purchased automatically and added to my account.

This is a more recent innovation that has, in my opinion, nailed shut the coffin of dividend reinvestment programs. For many years one needed to manually purchase whole shares only after accumulating enough cash through dividends. One advantage of DRiPs was that the program did this automatically, and purchases were made for whole and fractional shares. Now that discount brokers offer the same ability, this advantage previously unique to DRiPs is now common.

But Will It Last?

I asked myself this question when I first became aware that brokers offered everything the traditional DRiP offered. After all, I had seen the coming and going of companies like BuyAndHold.com, which initially offered free purchases, then charged monthly fees, and then went out of business.

Zecco is another broker that initially offered free stock purchases, then decided to charge. I am with Ally because I originally created an account with Zecco to get free trades, and Ally acquired Zecco, which eventually decided to go fee-free.

Things change over time. Small companies may attempt to build a business model on innovation, but oftentimes that model is either flawed or does not offer enough of a revenue stream to continue. Sometimes companies are just too early with their ideas. However, when the big boys make a change, like going fee-free, it becomes the standard, and I do not expect this to be changed any time soon.

The Biggest Problem With DRiPs

The major problem with DRiPs – and this existed when I first started participating in them – is that one can only enter a DRiP as a shareholder. That is a true barrier to entry.

Long ago, I wrote a series of articles that explained how to get a share, making entry into the program possible. To the uninitiated, purchasing shares through a broker does not make one an actual shareholder. When you purchase through a broker, the broker owns the share for you. The broker is the actual owner of the share.

If you want to become the actual shareholder, you need to request that a physical certificate be sent to you. Once obtained, you are the legal shareholder and become eligible to participate in the dividend reinvestment program. For years at DRiPInvesting.org, we kept track of discount brokers who would send the certificate for a small fee, but these days one is looking at around $100 to have a physical certificate mailed (if the service is even offered).

directinvesting.com used to offer a service that would make the initial purchase for you, and then enroll you in the company’s dividend reinvestment program. I have mentioned them many times and long ago used their service. However, now they are sending people to Temper of the Times, which I believe to be a spinoff of the company. I did not have the patience to read through all of the text on their website to figure out the actual cost of getting enrolled in the DRiP, so if you are interested, then have at it.

Canadians do not have as easy a time of this as we do in the United States. For this reason, I created a Share Exchange message board that was for their exclusive use, where participants could offer shares to other participants. If you use it, then do so at your own risk. The board is on Google Groups – when it was on DRiPInvesting.org, it was popular and successful, though one should understand that there can always be problems and disagreements.

Finishing Up

I still have four classic DRiPs from when I first started investing in this direction. I will be moving them over to Ally at some point soon. There is no major advantage to do so, besides the fact that instead of getting quarterly reports, I am now receiving yearly reports. Unless I log into Computershare's system, this information will be a mystery to me until January of next year, when they will send me the information for my taxes.

Not being one to worry or stress over the exact amount of shares I own, it is not a major issue. I do not have plans to sell and will almost certainly hold onto the shares for a long time, allowing them to accumulate over that time. On the one hand, it would be a bit more convenient to see all of my equities in one place. On the other, according to Dividend Growth Investor, a Fidelity study showed their best-performing investors to have been those who did nothing with their accounts.

I do not see any advantage a dividend reinvestment program has over holding a stock with a broker that succeeds in both of the two issues noted above. Actually, going the traditional DRiP route is time-consuming and more expensive, so yes, dividend reinvestment programs are dead.

Additional Resources

.jpg) Yup. This is one of those articles. It's an election year, and here in the U.S., we get to decide which old dude who’s been alive long enough to remember when there were only 48 states in the U.S. will be the leader of the free world.

Yup. This is one of those articles. It's an election year, and here in the U.S., we get to decide which old dude who’s been alive long enough to remember when there were only 48 states in the U.S. will be the leader of the free world. Reinvesting dividends could mean compound growth for your portfolio. But reinvesting them manually can be a hassle. This is why you could benefit from a dividend reinvestment plan (DRIP).

Reinvesting dividends could mean compound growth for your portfolio. But reinvesting them manually can be a hassle. This is why you could benefit from a dividend reinvestment plan (DRIP). We all know that in order to build wealth and prepare for retirement, investing is the key. However, it can be hard to figure out what to invest in and how to put your money to good use. One of the most talked about ways to build wealth is owning property and being a landlord to bring in passive income. But what if you don’t want to do that? You can still invest in real estate!

We all know that in order to build wealth and prepare for retirement, investing is the key. However, it can be hard to figure out what to invest in and how to put your money to good use. One of the most talked about ways to build wealth is owning property and being a landlord to bring in passive income. But what if you don’t want to do that? You can still invest in real estate! ESG (Environmental, Social, and Governance) has become a polluted word for many traders and investors - but that doesn't mean it's going completely away. Nor does that mean you can't profit from nature or sustainable practices. But there are some opportunities in the regenerative ag, conservation, and green real estate spaces.

ESG (Environmental, Social, and Governance) has become a polluted word for many traders and investors - but that doesn't mean it's going completely away. Nor does that mean you can't profit from nature or sustainable practices. But there are some opportunities in the regenerative ag, conservation, and green real estate spaces. The financial landscape is as vast as it is complex, woven with various types of instruments that cater to the myriad needs of traders and investors alike. Among these, futures contracts play a significant role, especially for those looking to hedge against risk or speculate on the price movements of assets.

The financial landscape is as vast as it is complex, woven with various types of instruments that cater to the myriad needs of traders and investors alike. Among these, futures contracts play a significant role, especially for those looking to hedge against risk or speculate on the price movements of assets. Turning $100 into six figures is a goal no one should realistically have. But it's the question you might ask yourself: Can it be done? Sure. Probable? It's less probable than winning the lottery, but technically still probable - like finding a needle in a haystack the size of Canada. But possible? Absolutely.

Turning $100 into six figures is a goal no one should realistically have. But it's the question you might ask yourself: Can it be done? Sure. Probable? It's less probable than winning the lottery, but technically still probable - like finding a needle in a haystack the size of Canada. But possible? Absolutely..jpg) As you may know, in Chinese culture, each year is marked by one of the creatures from the list of Chinese zodiac animals. February 10 will mark the start of the Year of the Dragon — the only mythical creature among the Zodiac animals.

As you may know, in Chinese culture, each year is marked by one of the creatures from the list of Chinese zodiac animals. February 10 will mark the start of the Year of the Dragon — the only mythical creature among the Zodiac animals. Looking for an investment calculator that you can download and keep on your desktop? You came to the right place!

Looking for an investment calculator that you can download and keep on your desktop? You came to the right place! Deciding where to invest your money can be overwhelming even when you’re only focusing on the United States. The question that inevitably comes up is, “should I invest outside the U.S.?” "And if so, how?" The search often leads people toward the best European index funds.

Deciding where to invest your money can be overwhelming even when you’re only focusing on the United States. The question that inevitably comes up is, “should I invest outside the U.S.?” "And if so, how?" The search often leads people toward the best European index funds.- Wondering how to buy VTI? And do you need a Vanguard account to buy VTI? These are common questions for new investors that either aren't familiar with ETFs, or they're just having trouble navigating Vanguard's website (and I don't blame you for that! I still get lost on their site once in a while!).

Investing in mutual funds, index funds, stocks, bonds, or real estate is sometimes so convoluted, many people give up. Even if you already know how to invest, where and how much can leave you second guessing yourself in the middle of the night.

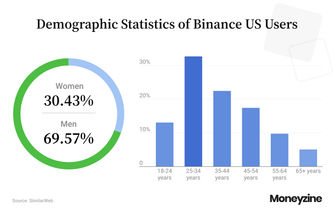

Investing in mutual funds, index funds, stocks, bonds, or real estate is sometimes so convoluted, many people give up. Even if you already know how to invest, where and how much can leave you second guessing yourself in the middle of the night. With its once-main competitor FTX out of the picture, Binance is undoubtedly the world’s best-known active crypto exchange. In this overview of Binance statistics, we’ll take a closer look at the company’s latest financial results and examine its user base. We’ll also explore Binance’s other endeavors, including venture capital, charity, and event organization. Finally, we’ll discuss Binance’s recent activities and the legal challenges it currently faces in the US.

With its once-main competitor FTX out of the picture, Binance is undoubtedly the world’s best-known active crypto exchange. In this overview of Binance statistics, we’ll take a closer look at the company’s latest financial results and examine its user base. We’ll also explore Binance’s other endeavors, including venture capital, charity, and event organization. Finally, we’ll discuss Binance’s recent activities and the legal challenges it currently faces in the US. Finance is a notoriously difficult industry to work in. There are long working hours, a high level of competition and usually involves a high-stress environment. However, even with all these challenges over 9.1 million people choose to work in finance roles all over America, according to the U.S Bureau of Labor Statistics (BLS).

Finance is a notoriously difficult industry to work in. There are long working hours, a high level of competition and usually involves a high-stress environment. However, even with all these challenges over 9.1 million people choose to work in finance roles all over America, according to the U.S Bureau of Labor Statistics (BLS).

.jpg)

.jpg)