Banks have been a solid choice for dividend investors. However, the Federal Reserve might make banks a less safe choice for investors.

The recession of 2008 came close to sending the country into a Depression. Banks purchased complex bundles of securities that turned out to be worthless, throwing the economic system into crisis. History.com provides a history of the recession, but of interest at this point has to do with the initiation of the Supervisory Capital Assessment Program (SCAP).

One of the more important elements of restoring the health of U.S. banks was the initiation of stress tests. Following the injection of capital into banks through the Troubled Asset Relief Program (TARP), the Treasury realized that giving additional capital to banks that were not able to have it provided through private sources would restore confidence in the system. To find out how much would be needed, the stress tests offered forward-looking determinations of revenues and losses for the largest banks and took the unusual step of making the results public.

Start with Interactive Brokers

Fast-forward a dozen years and the current crisis is due to the COVID-19 virus. The Federal Reserve performs stress tests every year, but due to the virus, this year’s test was different. They considered the extreme possibility of unemployment topping 19.5% and tested for three scenarios, a quick recovery, a slow recovery, and a recovery followed by a rebound of the virus. As a result of the results of the stress tests, they made three decisions for 33 large banks that apply to the third quarter of this year:

- Share repurchases are suspended

- Dividends are capped – no increases

- Dividends are allowed according to a formula based on the income of the four previous quarters

The issue of buybacks is not an issue at all, as large banks in March had already suspended repurchasing shares to preserve capital. The second item, however, is significant because banks tend to increase their dividend in the third quarter. This means that, at best, the dividend will remain the same. The third decision might affect banks that are on the borderline of being able to cover their dividend and may even be required to cut it.

Banks with exposure to mortgage payments may be the most affected, as under the CARES Act an abnormally high number of homeowners are not paying their mortgages. Auto loan and credit card forbearance weakens the capitalization of banks, and as this is the way they make money, delinquencies strike at a bank’s cash flow.

This puts into question what one should do if they happen to own bank stocks. It is certainly possible that a few of the 33 banks will lower their dividends. If one does not own any bank stocks then it may be time to take note of any drops of quality companies and see them as buying opportunities. However, this should be done with caution. Because of the stress tests, banks are much better capitalized than at the start of the last recession – levels of common equity capital are double that of 12 years back. Also helping is that the central banks have provided additional liquidity and capital, allowing banks to lend to small businesses.

FactSet’s estimation of second-quarter earnings helped create the below comparison of four-quarter estimated earnings averages and first-quarter dividends paid for the six largest banks.

| Bank and Ticker | Ave. Profit * | Div. ** | Div / Profit Ratio |

|---|---|---|---|

| J.P. Morgan Chase & Co. (JPM) | $5,968 | $3,188 | 53.00% |

| Bank of America Corp (BAC) | $4,999 | $2,083 | 42.00% |

| Citigroup Inc. (C) | $3,372 | $1,365 | 40.00% |

| Wells Fargo & Co. (WFC) | $2,207 | $2,312 | 105.00% |

| Goldman Sachs Group Inc. (GS) | $1,557 | $538 | 35.00% |

| Morgan Stanley (MS) | $1,909 | $688 | 36% |

| Values in Millions |

** First Quarter

As can be seen, Wells Fargo is the only bank where the dividends exceeded its estimated average net income. Following 9 years of dividend increases, Wells Fargo has reported that they are going to cut their dividend in the third quarter – the actual amount will be announced when they report their second-quarter earnings. The other five banks have said that they will retain their dividends for now.

This issue puts banking stocks into question. With loan losses potentially as high as $700 billion across the 33 banks being examined, the increased scrutiny could place some business decisions in the hands of regulators.

One of the Fed’s governors feels that all dividends should be suspended. Lael Brainard offered a statement that said. “Temporarily halting shareholder payouts … would create a level playing field and allow all banks to preserve capital without suffering a competitive disadvantage relative to their peers.” This is a minority opinion at this point.

The big banks will be required to resubmit updated capital plans for the year and additional stress analyses will be required. New “sensitivity” analysis protocols will be incorporated to examine capital levels for the three scenarios noted above. In a worst-case scenario that minority opinion could move to the majority.

What has been a safe dividend in the past (J.P. Morgan Chase and Goldman Sachs have 9 years consecutive dividend growth, Bank of America and Morgan Stanley 6 years, Citigroup 5 years) is now in question and it becomes the opinion of the Federal Reserve as to whether or not the increases, or even dividends themselves, can continue in the future. There may be bargains to be had, but one may wish to place more of an emphasis on growth than the dividend itself with future purchases.

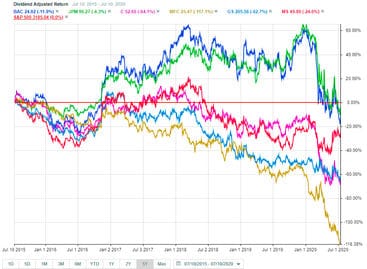

Looking at growth with a large bank is easier said than done. In the chart above Bank of America and J.P. Morgan Chase compared favorably against the S&P 500 over the past five years, but were brought back to earth by the pandemic. Despite Wells Fargo’s current (soon to be less) dividend yield of 8%, its returns dramatically lag the other five, perhaps a piece of data to be taken into consideration.

Finishing Up

Bank stocks have entered a realm of uncertainty not seen during the past decade. While the dividend is an important element in an investor’s decision-making process, it should be noted that going forward, at least in the immediate future, the decision on dividend amounts may have more to do with following Federal Reserve guidelines than the company’s business decisions.